Emil Waszkowski

VP of Commercial Development

What technology prompted Mark Zuckerberg to launch a team assigned only to its exploration ? What made Kodak's stock price go up by 60% in only a day ? What solves both ad fraud, distrust towards brands issues and the problem with personal data management? The answer to all above questions is Blockchain! Read this article to find out more about the benefits of applying this technology in business and marketing. But let's begin with explaining what blockchain actually is and why so many people are so interested in it?

Even if it's the first time you hear about blockchain you must have heard about cryptocurrencies, among which bitcoin is the most known. But I will not expatiate on the „Bitcoin fortune” topic (I don't know how to make it myself). I'm mentioning bitcoin because it is based on blockchain and its example is perfectly suited for explaining the whole technology.

Blockchain is a database containing chronological record register , which is co-owned by all its users . Just as the name implies it is all based records (transactions) saved in blocks that are linked by a chain , in which every component relies on the previous one . Every user can store a copy of the whole database . Thanks to that the base is fully decentralised and distributed . This solution prevents modifying, deleting and falsifying data . All blockchain users are equal and there is no one institution that serves as an administrator . This is possible thanks to the algorithm (protocol) that regulates how given blockchain works . All users can access the algorithm, which means any of them who possesses any programming skills can analyse and examine the protocol.

I know that it's not possible to understand how blockchain works when given only one definition. That is why I'll describe all blockchain features using a real example of money transfer. However, simplifications were unavoidable due to the fact that explaing all technical details would take several long articles.

Bitcoin and, along it, blockchain as we know it, came to existence at the beginning of 2009. Bitcoin creators wanted to enable direct and safe resource exchange without involvement of trusted middlemen (e.g. banks and other institutions that lost public trust after the financial crisis of 2008) that confirm every transaction and account balance with their authority. How were they able to manage that?... Wait, can't I do something similar myself? Yes, you can exchange cash, prepare a written agreement every time, run an offline transaction registry and store it all in a safe , but let's be honest, it is not an acceptable solution in the 21st century. Blockchain solves this issue much easier.

For blockchain to work at least three people who did not want to rely on banks were needed. What encouraged them to take part? They were told that they'll be able to mine (more on that later) given amount of bitcoin using very little computing resources.

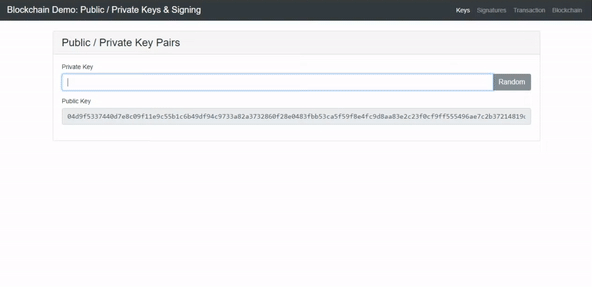

Keys

We have a group of people, now it's time for transactions. Unlike in the case of bank transfers we do not have to create an account and give its number or our name to receive a transfer. Instead we log in to a wallet e.g. coinbase or (one of the simplest) Coin .Space and receive an address containing numbers and letters e.g.

1BvBMSEYstWetqTFn5Au4m4GFg7xJaNVN2

This address is created based on two keys: private and public. First key is used to “sign” the transaction i.e. to confirm that you are the owner of a specific account in the bitcoin network. However, the public key is generated based on the private one and is an equivalent of a banking account (we can provide it to anyone who wants to send us money). Bitcoin wallets generate addresses automatically to make the process more convenient for the users and it is all they need to use bitcoins or other cryptocurrencies. I should mention the fact that for the purpose of preserving user anonymity new wallet address is generated for every transaction. What's important, based on a private key users can generate a public one, but not the other way around. Look below to see for yourself how (more or less) the keys are usually generated.

Source: https://anders.com/blockchain/public-private-keys/signatures.html

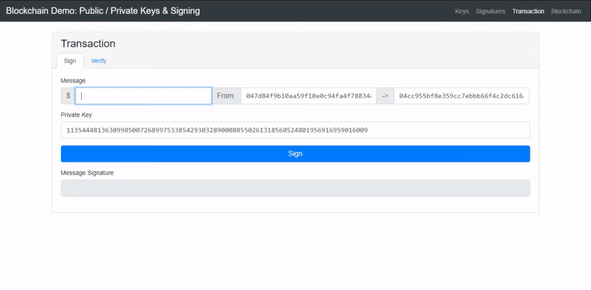

Transaction

Bitcoins can be best explained using the example of coinbase, which is used to connect a debit card to exchange dollars for bitcoins. User enters wallet address to send bitcoins to, clicks “confirm” and it's all ready. The magic takes place beneath the surface.

To confirm that you were the person performing a transaction you need to sign it by using private key linked to the wallet address. A unique transaction code is generated by linking the message (transaction) to a private key. If anyone would like to change anything in the key or transfer amount the code would change and the whole transaction would be invalid. After that transaction is signed and it is published in the network.

Source: https://anders.com/blockchain/public-private-keys/transaction.html

That doesn't mean however, that the whole operation is finished. Other users perform transactions the same way as described above, but someone has to manage transaction register. Without it you would be able to transfer the same bitcoin to two separate users (so-called “double spending”). There's no bank here, checking the account balance and preventing such situations. If there's no central institution then how is the register managed?

Transaction confirmation (mining)

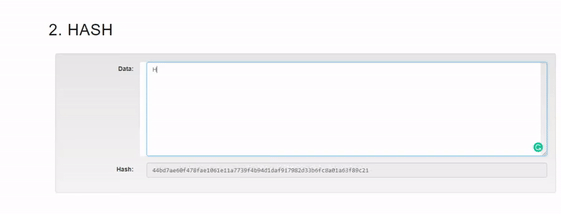

So how are the transactions checked and confirmed? They are collected by special blockchain users, so-called miners. They create a block by combining given amount of transactions. Then they solve a cryptographic puzzle to publish the block in the network, which serves the purpose of establishing order (consensus) in the decentralised network and prevents double spending.

Cryptographic puzzle is based on so-called hash function that adds a short fix-sized random value to any database, regardless of its size. The function is unique and there's no possible way to generate the same value for two different data entries. Even the slightest value modification would result in hash function change. If anyone would hash a book and change only one letter in it, it would result in hash function value change. The second important feature is the hash function irreversibility. It's not possible to use this function to generate a database that it had originated from. These features protect data from random or intentional changes.

Source: http://blockchain.mit.edu/hash/

Cryptographic puzzle requires (in case of Proof of Work consensus algorithm used by bitcoin network) finding missing block element (so-called “nonce”), so that when we hash it we'll receive a given amount of zeros at the beginning of the hash value. It's impossible to predict hash function value, therefore, the only way is to use an integer sequence, which will, by connecting to a specific block content, produce a hash number with e.g. 10 zeros at the start.

The amount of zeros is constantly changing and adapts to computing power of machines running the network (at the moment we are writing this article there are 18 zeros in bitcoin network). Why? To prevent transaction history modifications. In the case of bitcoin blockchain mining one block takes about 10 minutes. Of course, miners don't work for free, their reward for one mined block are bitcoins.

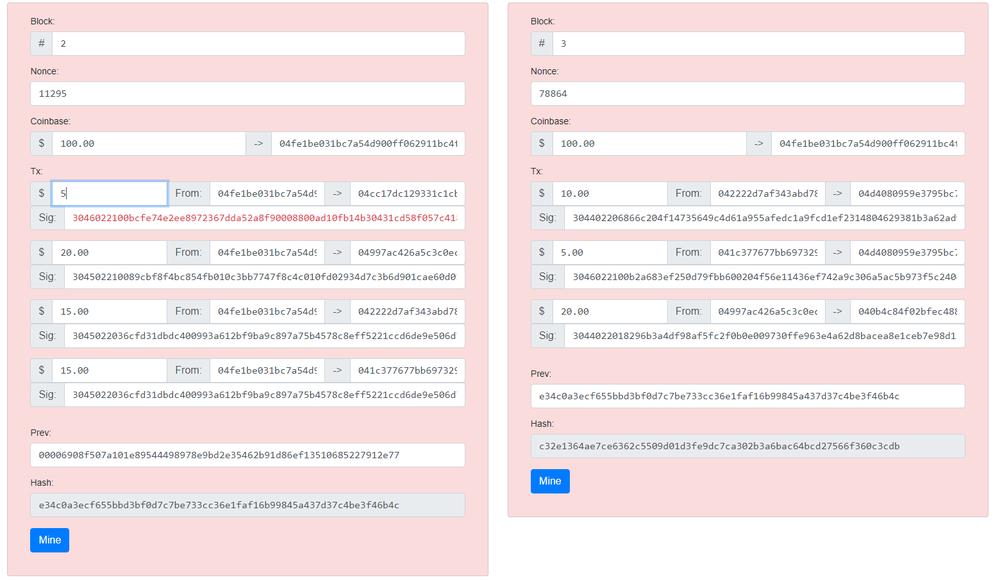

You'll find two transaction blocks below. Each contains a number, nonce value, transaction registry along with their codes, hash value or previous block hash. I tried to change block #2 single transaction value, which caused a change in this transaction code, as well as in the whole block hash. Because every next block shares its hash with the previous one, all consecutive blocks changed as well — this is what I meant by “ every component relies on the previous one ” in the definition part. To change transaction history someone would have to mine all blocks following the changed one (#2 in our example), but the network would still reject this version, because it's distributed — other users possess correct blocks and only the version with most users counts. On the graph below I've depicted a distributed blockchain. In this example the chain is distributed among two computers, but blockchain copies are placed on hundreds or thousands hard-drives all over the world. In the example below I've changed value of the first block in one copy. Despite that, second copy remained the same. If we assume that there are more copies network will accept a version present on most machines. That is why blockchain is considered unchangeable and irreversible.

Transaction blocks

Source: https://anders.com/blockchain/public-private-keys/blockchain.html

Distributed blockchain

Source: http://blockchain.mit.edu/distributed/

I've got yet two important terms left to explain. They'll become useful in the next part: smart contract and token . They were introduced along with Ethereum, which was the second blockchain milestone after bitcoin. Ethereum is a platform that allows smart contract and token creation. It has it's own currency (Ether), which serves as a payment transaction regulation when it comes to smart contracts and token fees. Thanks to Ethereum blockchain technology could expand outside the financial industry.

What's a smart contract?

Smart contracts are saved blockchain agreements that take a form of computer programs, based on IFTTT logic (IF-THIS-THEN-THAT) e.g. if a train is 30 minutes late you'll receive a 20% refund. In this example smart contract could download train travel time from transport company database and, in case of a delay, automatically send money to customer account. Without writing complaints, waiting for an answer and refund.

Hmm. Can't I manage it without blockchain? Yes you can, but there's no such agreement that cannot be broken or questioned, right? In case of smart contracts same rules apply as in bitcoin transaction explained above — once created, the contract is unchangeable and irreversible. It makes this deal self-executable.

Source: Blockgeeks

What's a token?

To explain what is a token I have to mention decentralised apps (DAPPs) — source programs built on blockchain and possessing its features. Ethereum and decentralised apps can be compared to the Internet and www pages. To build a DAAP you don't have to create a blockchain from scratch, Ethereum provides all necessary technology. One of the most interesting DAAPs is one created by a Polish brand called Golem. Its creators call it “Airbnb for computers”. Golem is a peer-to-peer network that allows users to rent unused computing power of their devices.

Tokens are tightly connected to decentralised apps. There are two token types with following functionalities:

You can read more on tokens and smart contracts here . This is a good place to mention that tokens can also store material assets. Everything can be “tokenised”: real estate, stocks, even yourself. Tokens can democratise investments, but law has to follow the technology. More on tokens and traditional assets here .

Let's move to the second question of this article. Technological development greatly influences marketing. From strategy planning, through execution, to analysis. Marketers can access countless data coming from distribution channels and tools they use to manage the whole process. Despite that, we are facing unprecedented distrust towards brands (which is caused mainly by fear of personal data leakage) or product authenticity concerns. Fake news, mass personal data leakage (or making it available to third parties) and other similar phenomena further increase distrust. According to a survey conducted by CB Insights its respondents believe that among the biggest technological companies Facebook will have the biggest negative influence on society in the next 10 years .

From the business operation perspective we are challenged by ineffective ad cost analysis, caused by bot traffic and many middlemen in the ad supply chain. According to Forrester agency study, advertisers lost 7,4 billion dollars in 2016 due to ad fraud . What's more, Forrester predicts that losses may reach 10,9 billion dollars in 2021. Video and programmatic ads are the ones most threatened by fraud. Due to a large scale of abuse the problem seems to grow beyond marketing departments. According to CMO Council report 72% CMOs are under pressure by their CEOs to solve problems concerning trust between brands, agencies, publishers and clients .

Thanks to its features — transparency, irreversibility and immutability — blockchain works like a trust machine , and that is why it can be applied whenever two parties exchange something and want a good method to do it while establishing trust and transparency. Let's take a look then, on how to make use of blockchain qualities to solve above problems. I'll present blockchain application examples coming from Walmart, AXA and similar companies, as well as ideas that may help you take advantage of this technology.

1. Increase trust towards a brand — thanks to previously mentioned smart contract features (irreversibility and immutability) you can use it to prove product quality and guarantee pledge fulfilment.

Supply chain control is a flagship example. Blockchain enables safer and faster cooperation between all chain users: from suppliers, through shippers, producers and retailers.

Let's say that you want to guarantee quality and safety when it comes to vegetables sold by your chain store. To find out if the producer cultivates them accordingly, you consult a certain quality assurance institution (a kind of a middleman) that has to be paid. You also have to trust the carrier to transport your goods in the right conditions e.g. in the right temperature.

How can you change all that? You create a smart contract with your producer. You write down conditions that you require the vegetables to be cultivated in and what data source you'll use to confirm that e.g. IoT hydration sensor on the plantation. If a batch is hydrated according to contract, auto-payment is activated in set time period. This process makes you free of an outside institution, otherwise needed to ensure quality. The same goes for transport. You agree on e.g. transport temperature in your contract (IoT thermometer provides necessary data). If the temperature does not exceed agreed value, auto-payment is activated. Final customer can access smart contract and check if the product they buy is up to standards. Read more on how Walmart and Maersk use blockchain to increase safety and reduce transport costs .

What about the case when your product is damaged or the service is not provided according to the agreement? I imagine an intelligent contract warranty. Service will be provided based on trusted data sources — database, API, IoT sensors or authorised service. This warranty (or insurance) cannot be breached, there is no escape from fulfilling your obligations.

It's still too soon to introduce such solution on a mass scale but a pilot programme can bring you valuable data and benefit your PR. Read about AXA's smart contract tests .

2. Preventing fraud in online advertising . Marketing industry faces distrust and too-many-middlemen problems. You should know by now that blockchain can help with those issues. Software developers working on decentralised apps know that as well, which is why more and more projects are made. Take a look at two examples:

You're thinking “Ok, they want to remove middlemen but they are middleman themselves, how do they want to profit from that?" I've been wondering about that too. It's all true, but they offer much lower rates in a form of tokens worth 1% of the ad price compared to 30-50% in case of centralised middlemen.

3. Managing personal data — blockchain can change the way how we manage our online data. Specific websites and apps currently collect data about our activity and use it for ad-related purposes. The result is that users do not own their data. Developers want to change that by creating decentralised apps that will work like a cryptographically locked wallet, allowing its owners to decide with whom and for what purpose they share all collected info. The wallet will contain personal data as well as data collected while users are using social media. Therefore, data that can be downloaded from your Google, Apple or Facebook accounts can be collected in an anonymous form in one wallet and you can decide who has access to it. Civic is a good example of utilising blockchain to that purpose.

There is an equally interesting app, built by Mozilla's co-founder — Brave browser . It allows users to block all ads and cookies, and enables them to support their favourite websites or content creators with micropayments in cryptocurrencies, instead of watching ads. The next step is getting paid for watching an ad — users will be rewarded for interacting with specific ads. This functionality is developed by Brave creators. Thanks to apps like this creators and publishers will be forced to improve their content quality to convince users to give access to their data.

4. Social media . Solutions mentioned above will also influence social media. This is the part where I answer the question from the introduction — how can Facebook utilise blockchain? My answer is: It can employ this technology for its daily operations as well as for improving value for its users. Here is what they can do:

In today's world customer trust can be earned by offering value and transparency, As of this moment blockchain guarantees mainly the latter thanks to its technology as well as white paper publishing, containing app description, its vision and mission. Currently user value innovation is not yet strong enough to apply blockchain applications on a large scale, but it's a good moment to be launching pilot projects that will not only help you gain experience but also bring good PR. Don't forget to create a lucid product presentation and remember to explain what blockchain actually is while you're taking it on.

In marketing tools and services sector this technology can be adapted much faster than in the other fields. The financial industry shows us that this prediction can be very much true. However, projects that I mentioned in this article are still in development phase. In the coming year their creators must prove value and reliability of their software.

This is just the beginning of blockchain development (current state of this technology can be compared to the Internet in the first half of the 1990's), so it's still hard to predict how will it grow, maybe it will not stand the test of time? When the first iPhone was introduced we did not think we were going to rent cars with a mobile app. That is why we do not know all the answers, what's more, we do not even know all the questions. Blockchain is not a technology that you have to implement right now, but it's good to know what it is, what value can it bring to your business and what should be done about it at this moment. That is what I wanted to share with you in this article.

Originally published in Polish by NowyMarketing .

M. Cieślukowski - Senior UX Researcher

I. Franke - Head of Advisory

K. Borowiec - Business Development Manager

J. Nawrocki - Lead UX Researcher , I. Franke - Head of Advisory